Mortgage-Backed Securities (MBS) in 2024 - What to Think and How to Respond

- Jonathan Poyer

- May 17, 2024

- 2 min read

The rally across risk assets at the end of 2023 spilled over into Q1 2024 as many equities continued to march higher. Mortgage rates, which tend to track the Treasury bond market, were roughly flat at 6.75%, although jumbo rates narrowed given credit spread tightening in non-Agency RMBS.

In the RMBS market, credit spreads generally tightened across different types of mortgages and positions in the capital structure. Within non-Agency RMBS, mezzanine securities experienced more pronounced credit spread tightening compared to more senior securities.

Non-QM AAAs tightened ~20 bps while SFR (Single Family Rental) and RPL (Re-Performing Loans) AAAs both tightened ~50bps. Prices for mezzanine CRT and Non-QM bonds were bid up in varying degrees depending on coupon type and amount of credit support.

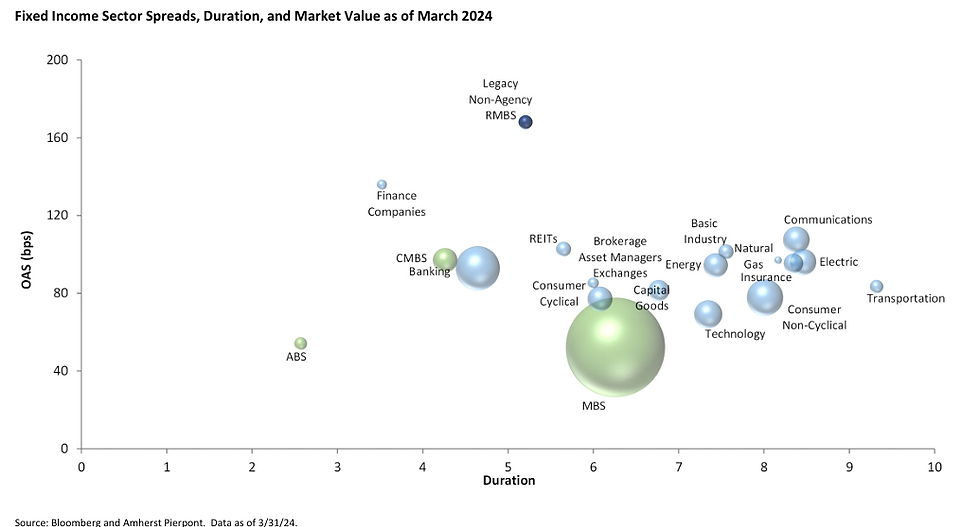

Generally, insurance companies and money managers exhibited strong demand for non-Agency RMBS given the perceived strong fundamental backdrop and enticing yields versus other parts of the market. On the Agency (government guaranteed) MBS side, the basis (or spread over Treasury bonds) was a bit less volatile versus the previous quarter. The nominal spread ended 1Q2024 at ~142bps (roughly unchanged from Q42023) although in mid-February the spread touched ~160bps. In our opinion, the two major factors weighing on Agency MBS spreads are the Fed’s absence from the market and uncertainty over the fate of several banks.

Wide Agency MBS spreads are also a major driver of a relatively flat “credit curve” in the non-Agency RMBS market. Spreads for senior RMBS bonds remain stuck at relatively wide levels as traders are reluctant to bid bonds at tighter credit spreads versus agency MBS trades.

Also, part of the decline will likely be from the tightening of the “basis” between Agency MBS and Treasury yields which remains wide relative to the historical average.

While we wouldn’t bet on significant home price appreciation in the short term, we believe the way to play stability in the housing market is by investing in certain RMBS, corporate credit, and mortgage related equities.

Comments