Agency Mortgage-Backed Securities: An Often-Overlooked Foundational Element of Retirement Income

- Michael Flaherty

- May 19

- 4 min read

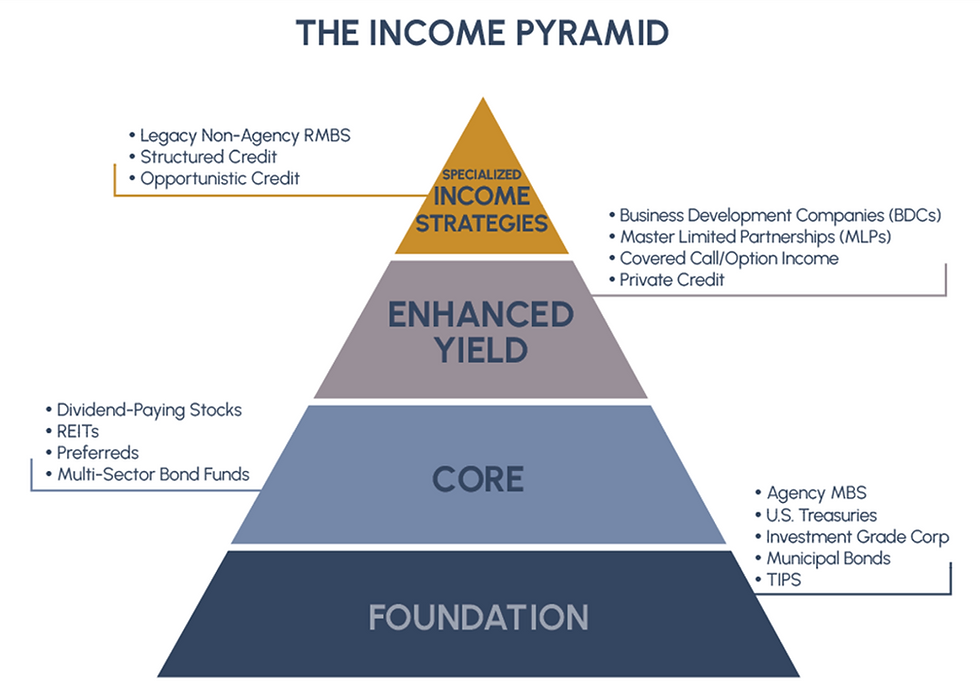

As we built the foundation of the retirement income pyramid, we focused first on the most familiar building blocks:

U.S. Treasuries,

investment-grade corporates,

municipal bonds,

and TIPS.

Those sectors form the backbone of many retirement portfolios because they emphasize stability, income, liquidity, and capital preservation.

But there is another major fixed-income sector that institutional investors have long considered foundational — even if retail investors hear far less about it: Agency Mortgage-Backed Securities (MBS).

In some ways, Agency MBS were intentionally saved for later in the discussion because they introduce slightly more complexity than traditional bonds. Yet that complexity should not obscure their importance.

In fact, Agency MBS may be one of the most underappreciated foundational income assets available to retirees today.

1. What Are Agency Mortgage-Backed Securities?

Agency MBS are bonds backed by pools of residential mortgages.

When homeowners make monthly mortgage payments, those cash flows are passed through to investors who own the securities.

Most Agency MBS are issued through government-sponsored entities (GSEs) such as:

Ginnie Mae,

Fannie Mae,

and Freddie Mac.

Because these are backed by US Gov’t agencies, the underlying credit risk is considered very high quality relative to many other fixed-income sectors.

Rather than lending to a single borrower, investors gain exposure to thousands of homeowners across diversified mortgage pools.

2. Why Agency MBS Matter in Retirement Income

Agency MBS have long occupied a central role in institutional fixed income portfolios because they combine several attractive characteristics:

High Credit Quality

The agency backing structure gives the sector strong credit characteristics.

Incremental Yield

Agency MBS have historically offered higher yields than comparable U.S. Treasuries.

Diversification

Mortgage cash flows behave differently than corporate bonds and Treasuries.

Large and Liquid Market

The Agency MBS market is one of the largest and most liquid bond markets in the world.

Broad Institutional Ownership

Banks, pension funds, insurance companies, mutual funds, and even the Federal Reserve have historically maintained substantial exposure to Agency MBS.

For retirees seeking stable income, these characteristics can make Agency MBS a compelling complement to other foundational holdings.

3. Why Agency MBS Can Be Harder to Understand

Unlike traditional bonds, mortgage-backed securities contain an unusual feature: homeowners can refinance or repay their mortgages early.

That means Agency MBS investors face two unique dynamics:

Prepayment Risk

When interest rates fall, homeowners may refinance, causing investors to receive principal back sooner than expected.

Extension Risk

When rates rise, refinancing slows, potentially extending the life of the bond.

This behavior creates what fixed-income investors call “negative convexity,” meaning Agency MBS can react differently to changing interest rates than traditional bonds.

That complexity is one reason the sector is often discussed less frequently in retail retirement conversations — even though institutional investors consider it a core allocation.

4. Why the Sector Looks Especially Interesting Today

The current environment may be one of the more attractive setups for Agency MBS in years.

Several forces have reshaped the market:

Higher Mortgage Rates Reduced Refinancing Risk

Most homeowners today carry mortgage rates far below current market rates, making refinancing activity unusually low.

Strong Underlying Homeowner Credit

Consumer balance sheets and homeowner equity positions remain historically strong.

Attractive Spreads

Agency MBS spreads versus Treasuries remain wider than long-term averages in many parts of the market.

Reduced Federal Reserve Support

After years of heavy Federal Reserve buying during quantitative easing programs, private investors are once again demanding more attractive compensation to own mortgages.

For long-term income investors, this combination has improved the sector’s prospective income profile.

5. Where Agency MBS Fit in the Income Pyramid

Agency MBS belong firmly in the Foundation layer of the retirement income framework.

Why?

Because their primary role remains:

income stability,

high-quality fixed income exposure,

diversification,

and capital preservation.

Although Agency MBS contain more structural complexity than Treasuries, they are still fundamentally high-quality bond instruments rather than economically sensitive equity assets.

In many diversified bond portfolios, Agency MBS act as a middle ground between:

the safety of Treasuries,

and the higher yields of spread sectors like corporate credit.

6. How Much Might a Retiree Own?

Most retirees gain Agency MBS exposure through:

core bond funds,

intermediate bond strategies,

multi-sector income funds,

or professionally managed fixed-income portfolios.

Direct allocations vary widely depending on:

interest rate outlook,

risk tolerance,

income needs,

and overall portfolio construction.

A retiree may not necessarily need a dedicated standalone Agency MBS allocation, but understanding the role mortgages play inside diversified bond portfolios can be extremely valuable.

For many investors, Agency MBS already represent a meaningful portion of their fixed-income exposure — whether they realize it or not.

7. Final Thoughts

Agency MBS are a reminder that some of the most important investment sectors are not always the most widely discussed.

While Treasuries, municipals, corporates, and TIPS often dominate retirement income conversations, Agency MBS have quietly served as a cornerstone of institutional fixed income investing for decades.

They offer:

high-quality income,

diversification,

liquidity,

and historically attractive risk-adjusted yields.

And in today’s market environment, the sector may be more compelling than many investors appreciate.

With Agency MBS, we conclude the Foundation layer of the retirement income pyramid:the stable base designed to support predictable income, capital preservation, and portfolio resilience.

From here, the conversation naturally shifts toward the Core layer — assets that begin introducing greater income potential, inflation sensitivity, and long-term growth opportunities alongside the stability built by the foundation beneath them.

Comments