Banking & Commercial Real Estate - What Is at Stake?

- Jonathan Poyer

- Mar 29, 2023

- 2 min read

Small- and medium-size banks play an important role in the American economy. Lenders with less than $250 billion in assets account for roughly 50% of U.S. commercial and industrial lending, 60% of residential real estate lending, 80% of commercial real estate lending and 45% of consumer lending, according to a report by Goldman Sachs economists Manuel Abecasis and David Mericle (Stress Among Small Banks is Likely to Slow the US Economy (goldmansachs.com)).

According to the FDIC (Historical Bank Data (fdic.gov)), there are over 4200 commercial banks in operation.

So...how does this impact you and your investments?

Regional banks mostly do not mark to market their loans and bonds which creates asset liability mismatches. Very large banks are forced to take into account at least some mark to market effects on capital ratios. TThus, the market is likely to uncover additional regional banks that have unsafe tangible capital ratios. If your bank is offering 50bps interest on a savings or checking account while a 10-year treasury (risk free asset???) is offering you 3.38% (3/23/2023) the odds are that depositors are going to withdraw capital from the bank.

Commercial real estate, which accounts for 43 per cent of small bank loans in the U.S., would be the most affected if banks continue to rein in lending to cope with a flight in deposits.

Small banks provide the lion’s share of commercial real estate lending, with $1.9 trillion in such loans outstanding, more than double the $900 billion held by big banks. Without small banks, commercial real estate borrowers would be hard-pressed to find other sources of funding. Pension funds and sovereign wealth funds are a possibility, but would institutions want to take on that risk considering that commercial property values are falling? Highly leveraged commercial real estate always struggles when interest rates are high, and it now faces even more headwinds as the rise of remote work and online retail sales sap demand for office and store space.

Think about this another way: there is about $1.5T in commercial real estate maturing in the next 3 years. The majority of this debt was financed when base interest rates were near zero. This debt will need to be refinanced in an environment where rates are higher, property value is lower, and where liquidity is drying up.

The market for CMBS, where banks bundle the loans and resells them to investors is struggling. Sales of these deals were down 85% in February compared with last year (Sales of CMBS Plunge 85% as Commercial Property Markets Freeze - Bloomberg). Only about $4.27B of the bonds have been issued down from $29.38B at this same point last year.

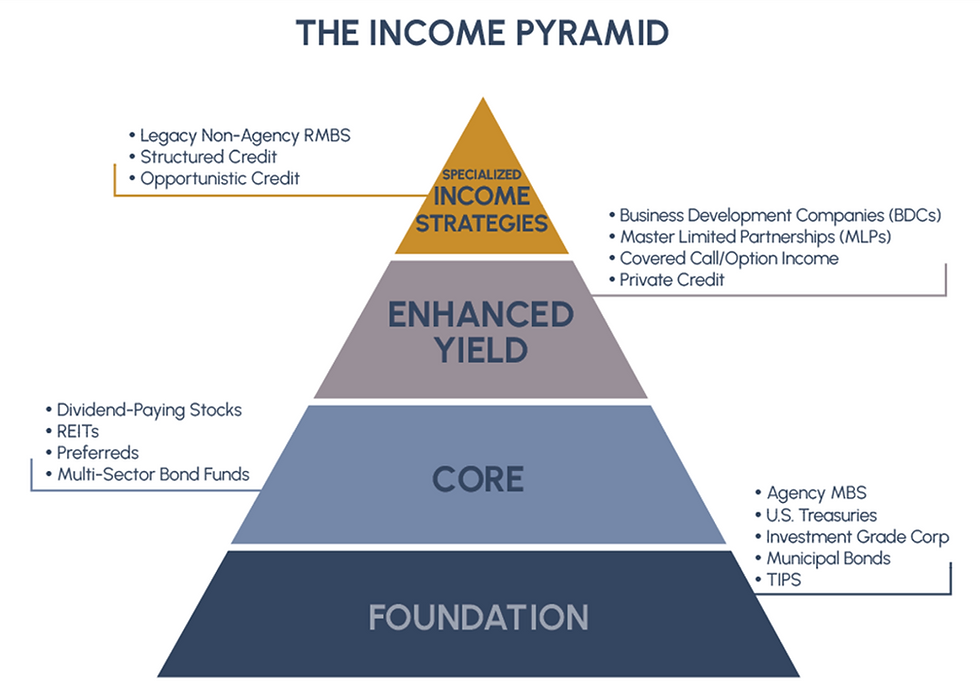

Are there pockets in the vast real estate market for investors to participate? Here are a few ideas that might be worth consideration:

Non-bank mortgage servicers and REITs have to mark all of their loans and bonds to market every quarter

Mortgage REITs are not banks and do not have deposits

Residential mortgage credit remains fundamentally solid and discounts to book value for mortgage REITs exceed 30% in some cases

Many mortgage related equities have diversified funding sources (securitization being a big one) and do not rely on short-term borrowing

Comments