If Biotech Is Near Rock Bottom, there is No Place to Go but Up

- Jonathan Poyer

- Nov 21, 2023

- 3 min read

The S&P Select Biotech Index managed to trade above the 50-day moving average as the 10 year yield remains below 4.50%.

Fed funds futures continue to project YE 2024 rates to be ~4.50% as the debate continues on how long will we be this high.

Vertex (VRTX) and CRISPR Therapeutics (CRSP) reached the historical milestone of the first regulatory authorization of a CRISPR-based gene-editing therapy anywhere in the world. The UK’s MHRA issued a conditional marketing authorization for CASGEVY (Exa-Cel) for the treatment of sickle cell disease (SCD) and transfusion-dependent beta thalassemia (TDT). FDA's review decision is expected in early December. CRSP shares are up >75% since the start of November and now sport a ~$6 billion market cap despite a ~$1 million per day cash burn rate. Time will tell is CRSP ends up being another short the launch casualty as many other commercial companies with approved drugs and $1 billion+ peak sales estimates are trading at depressed valuations.

WeWork's bankruptcy filing last week was a shot across the bow for all biotechs that even a $47 billion unicorn will perish if the business model is unable to produce cash flows over time.

Bayer (BAYN GY) posted its worst day in its 70 year history as a public company, falling nearly 20% on mounting damage awards related to litigation for weed killer Roundup (acquired in Monsanto deal) and the discontinuation of late stage anti-thrombotic factor XI drug asundexian that was expected to be a blockbuster for the pharma division. The IDMC (Independent Data Monitoring Committee) recommended stopping the 19,000 patient OCEANIC-AF phase 3 study evaluating asundexian in stroke prevention and systemic embolism in patients with atrial fibrillation due to a lack of efficacy. BAYN shares are now trading at nearly half the $63 billion they paid to acquire Monsanto in 2018.

Bristol Myers (BMY) was down in sympathy, notching a new 52 week low as their own factor XI program was assumed to be higher risk based on BAYN's failure.

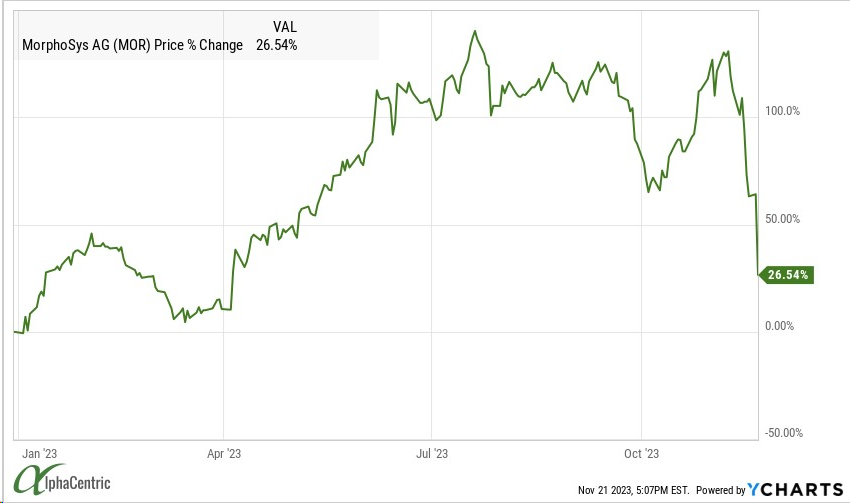

German biotech was under further pressure as Morphosys (MOR) traded lower upon announcing the highly anticipated MANIFEST-2 trial of BETi pelabresib in myelofibrosis hit the primary endpoint, but failed to meet a key secondary endpoint. Ironically, MOR shares are now trading at less than half the $1.7 billion cash they paid to acquire pelabresib in the deal for Constellation Pharmaceuticals.

2Seventy Bio (TSVT) continued to punish investors by announcing FDA will conduct an advisory committee meeting for cell therapy Abcema and will not have a decision in time for the scheduled December 16th action date. Insider purchases began to hit the wires as blackout periods related to quarterly reporting come to an end.

Management purchases at Apyx Medical (APYX), Kronos Bio (KRON) and Tandem Diabetes Care (TNDM) were generally well received. Investors have also been stepping up insider purchases as holders of negative enterprise value (EV) companies fight back against punitive price action.

Shares of Kinnate Biopharma (KNTE) rallied as a holder submitted a non-binding expression of interest to evaluate a potential acquisition.

Negative EV company Homology Medicines (FIXX) and Q32 bio entered into an all stock merger and financing to extend the cash runway to mid-2026. \

Likewise, Graphite Bio (GRPH) and LENZ Therapeutics are set to merge, leaving the pro forma business with $225 million in cash including $54 million concurrent PIPE.

Creative destruction continued with negative EV company Atreca (BCEL) laying off 40% of employees.

Biotech investors can at least be thankful rock-bottom valuations are often a precursor to meaningful upside

Comments