Housing in the Spring - Supply/Demand

- Jonathan Poyer

- May 21

- 2 min read

After creeping down to a low of 5.99% at the end of February, the 30-year mortgage rate now stands at 6.67%.

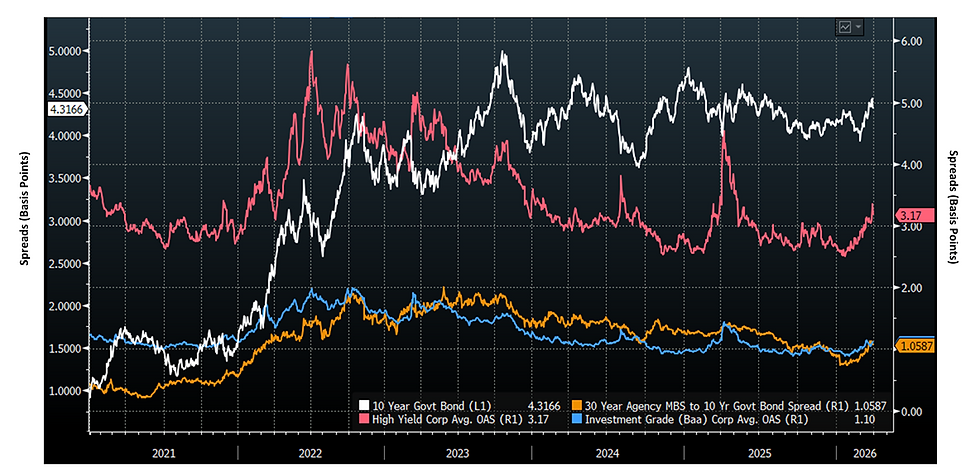

Rates and rate increase surely impact the fixed income market across the board. Although that impact varies based upon duration. Fixed income spreads between investment grade and high yield bounced off of January lows in March. Agency MBS spreads moved lower after the administrations announcements but have since widened.

We like to keep track of yield to maturity measures and spreads. Here is a comparison from 2022 through March 2026:

Overall, the RMBS sector is in pretty good shape. Especially if you consider the seasoned/legacy sub-sector. The more collateral, the better.

In the short-/near-term:

Fannie and Freddie purchases - sideways/delayed impact

Institutional home buyer limitation - sideways/delayed impact

New Fed Chair - sideways/delayed impact

This year:

Essentially no cuts priced

Inflation drop along with productivity gains - oil price impact

Lower rates - expected to resume

Excess spread benefits could manifest in bonds continuing 2025 strength

Potential outperformance of RMBS vs. other sectors.

U.S. Mortgages near lowest delinquency levels in 20 years. They are the lowest out of all loan types, making up just 2.4% of all 90+ delinquent loans.

Consumers are running out of options. Look at the aggregate personal savings compared with the pre-pandemic trend.

Cumulative aggregate pandemic-era excess savings.

Digging into housing, the percent of U.S. homes for sale was 0.7% of total U.S. housing, near the lowest level in nearly 5 decades. U.S. housing supply shortage is still significant.

Overall, legacy housing remains of great interest. Even if rates increase in the short-term because of energy concerns and wars, we still see the real asset for folks who have been in their homes for year as about the best place to be. Let alone the structural benefits in the MBS structure.

Comments