REITs: Turning Real Estate Into Retirement Income

- Michael Flaherty

- May 27

- 3 min read

What is a REIT and should you invest... Continuing the AlphaWatch retirement blog series.

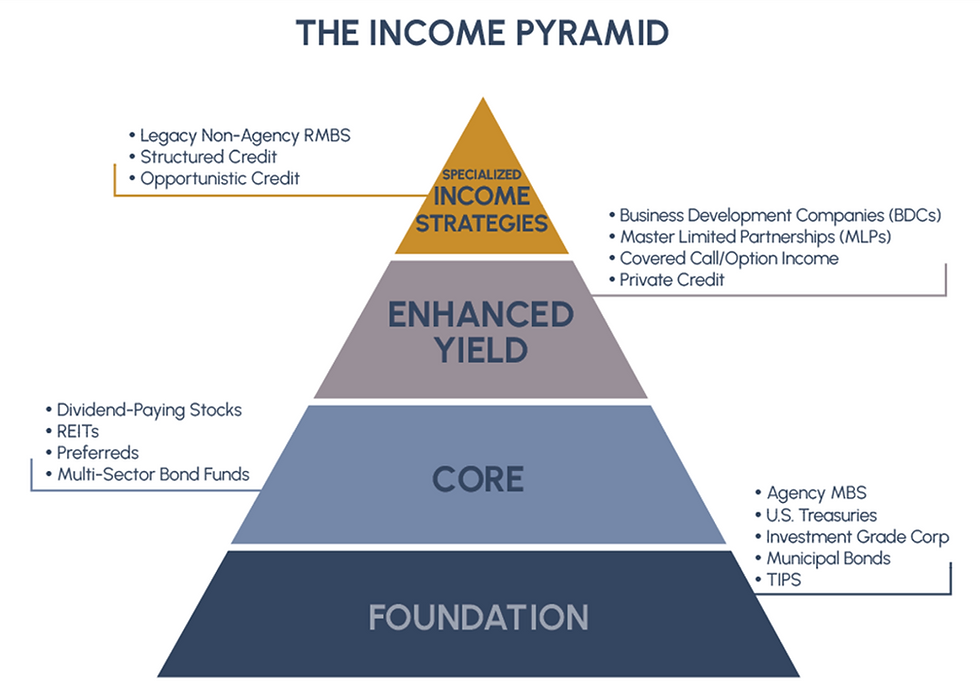

The Core Layer of the Retirement Income Pyramid

In the foundational layer of retirement income, we focused on stability: U.S. Treasuries, municipal bonds, investment-grade corporates, TIPS, and agency mortgage-backed securities. Those assets are designed first and foremost to preserve capital, provide dependable cash flow, and reduce portfolio volatility.

But retirees also face another challenge: income must grow over time.

That is where the Core Layer comes in.

Core assets seek to provide:

Higher income potential

Some inflation protection

Long-term cash flow growth

Diversification beyond traditional bonds

One of the most important components of this middle layer is the Real Estate Investment Trust, or REIT.

1. What Is a REIT?

A REIT is a company that owns, operates, or finances income-producing real estate.

Instead of buying an apartment building, shopping center, warehouse, or data center yourself, a REIT allows you to own a diversified portfolio of properties through publicly traded shares.

In many ways, REITs transform large-scale commercial real estate into a liquid income investment.

By law, most REITs must distribute at least 90% of taxable income to shareholders, which is why the sector has historically offered attractive yields.

REITs may own:

Apartment communities

Industrial warehouses

Office buildings

Healthcare facilities

Self-storage properties

Hotels

Shopping centers

Cell towers

Data centers

That last point is important. Modern REITs are no longer simply “malls and office buildings.” Many now own critical infrastructure powering the digital economy.

2. Why REITs Matter for Retirees

Retirees often need income that can keep pace with inflation over long periods of time.

Traditional bonds typically provide fixed payments. Real estate, however, has the potential to increase rents and property values over time.

That means REITs can offer:

Attractive current income

Potential dividend growth

Partial inflation protection

Diversification from stocks and bonds

In many cases, rental income adjusts upward over time as leases reset and property demand changes.

For retirees, this creates the possibility of an income stream that evolves rather than remaining static.

3. The Different Types of REITs

Not all REITs behave the same way. Property type matters enormously.

Equity REITs

These own physical real estate and collect rent.

Examples include:

Apartment REITs

Industrial REITs

Healthcare REITs

Data center REITs

Self-storage REITs

These are typically the preferred structure for long-term retirement investors.

Mortgage REITs (mREITs)

Mortgage REITs invest in real estate debt rather than buildings themselves.

They often offer very high yields but can be substantially more sensitive to:

Interest rates

Financing conditions

Credit spreads

Leverage

Because of this, mortgage REITs are usually considered more tactical and higher risk than traditional equity REITs.

Hybrid REITs

These combine elements of both property ownership and mortgage investing.

4. The Advantages of REITs in a Retirement Portfolio

Income Potential

REITs have historically provided yields above the broader equity market.

Inflation Sensitivity

Real estate income can adjust upward over time through rent increases and property appreciation.

Diversification

REIT returns are influenced by property fundamentals, occupancy trends, and lease structures—not just corporate earnings cycles.

Accessibility

Investors gain exposure to institutional-quality real estate without directly managing properties.

Professional Management

REITs employ teams focused on:

Acquisitions

Leasing

Financing

Property operations

Capital allocation

This allows retirees to participate in large-scale real estate ownership without becoming landlords.

5. The Risks Retirees Should Understand

REITs are not bond substitutes.

Although they generate income, they are still equities and can experience meaningful volatility.

Key risks include:

Interest Rate Sensitivity

Higher rates can pressure REIT valuations and financing costs.

Economic Cycles

Weak economic conditions can reduce occupancy and rental growth.

Sector-Specific Risks

Different property sectors behave differently:

Office properties may struggle during remote-work trends

Hotels can be economically sensitive

Retail properties face e-commerce competition

Healthcare properties may depend on reimbursement environments

Leverage

Real estate often relies on debt financing. Excess leverage can magnify downturns.

For retirees, quality and balance-sheet strength matter greatly.

6. How Much Might a Retiree Own?

REIT allocations vary widely depending on:

Income needs

Risk tolerance

Other equity exposure

Inflation concerns

Overall portfolio objectives

A common range might look something like this:

Investor Type | Typical REIT Allocation |

Conservative | 5–10% |

Moderate | 10–20% |

Growth-Oriented Income | 15–25% |

For many retirees, REITs work best as a complement to foundational fixed income—not a replacement for it.

The foundation provides stability. The core provides growth and enhanced income potential.

Together, they create balance.

7. Final Thoughts

REITs occupy an important middle ground in retirement portfolios.

They are not as stable as Treasuries or high-quality bonds, but they can provide something foundational assets often cannot: growing income tied to real-world assets.

That combination of:

Current cash flow

Inflation sensitivity

Long-term income growth

Real asset exposure

Makes REITs one of the most valuable components of the Core Layer of a retirement income strategy.

For retirees seeking to build resilient income streams over decades—not just years—real estate can play a meaningful supporting role inside a properly diversified portfolio.

Comments